Back to Blog

Predicting the Fed’s actions for fun and profit

What’s the federal funds rate

Is this the best we can do

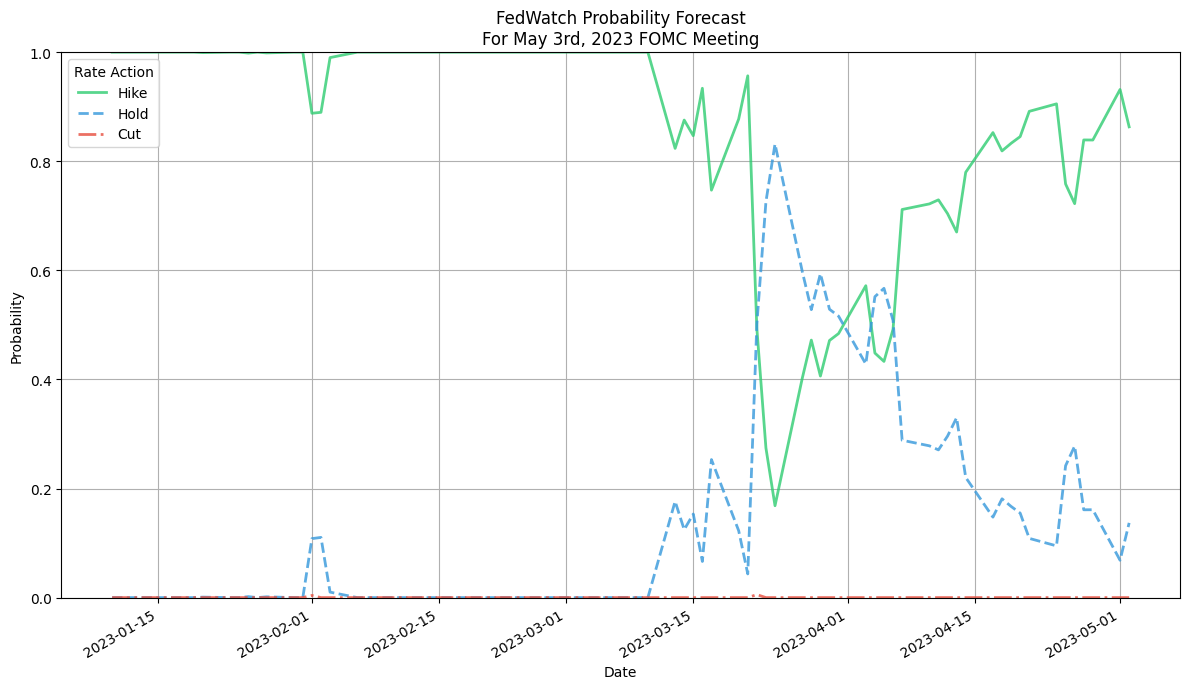

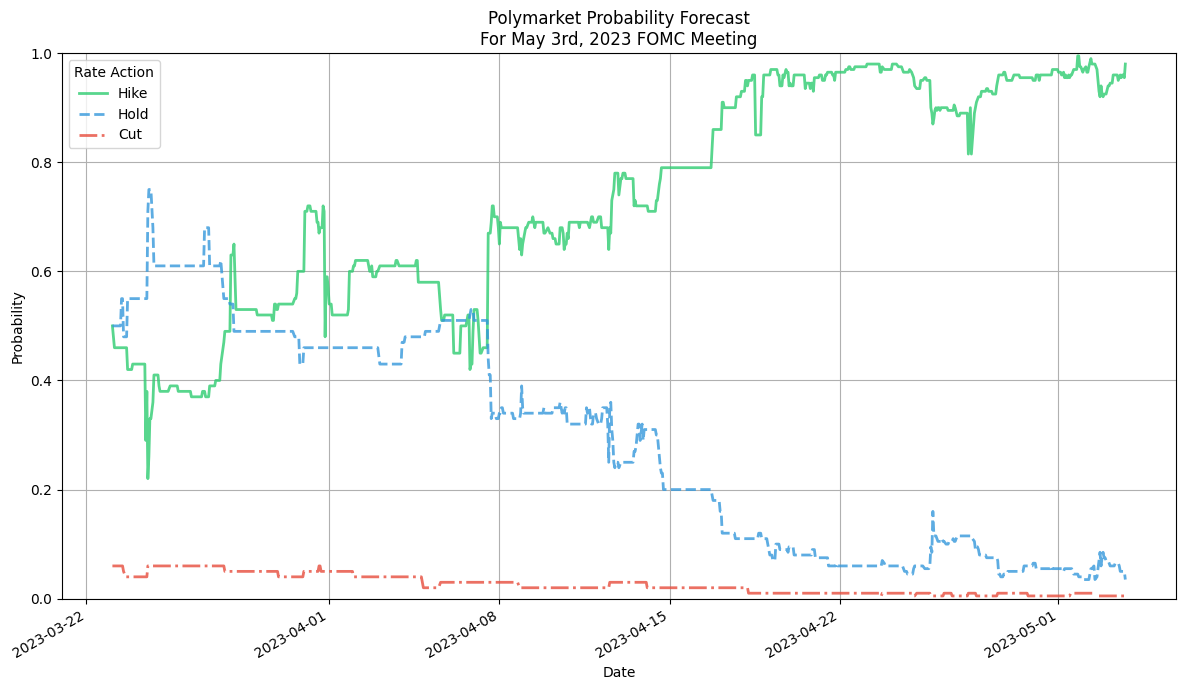

Data digging

| Days to meeting |

No. meetings covered |

Mean accuracy |

Mean confidence |

| 10 |

18 |

1.0 |

0.95 |

| 20 |

18 |

0.94 |

0.89 |

| 30 |

18 |

1.0 |

0.86 |

| 40 |

18 |

0.94 |

0.89 |

| 50 |

19 |

0.88 |

0.86 |

| 60 |

19 |

0.83 |

0.85 |

| Days to meeting |

No. meetings covered |

Mean accuracy |

Mean confidence |

| 10 |

18 |

1.0 |

0.94 |

| 20 |

18 |

0.94 |

0.88 |

| 30 |

17 |

1.0 |

0.85 |

| 40 |

17 |

0.93 |

0.84 |

| 50 |

9 |

1.0 |

0.78 |

| 60 |

6 |

1.0 |

0.72 |

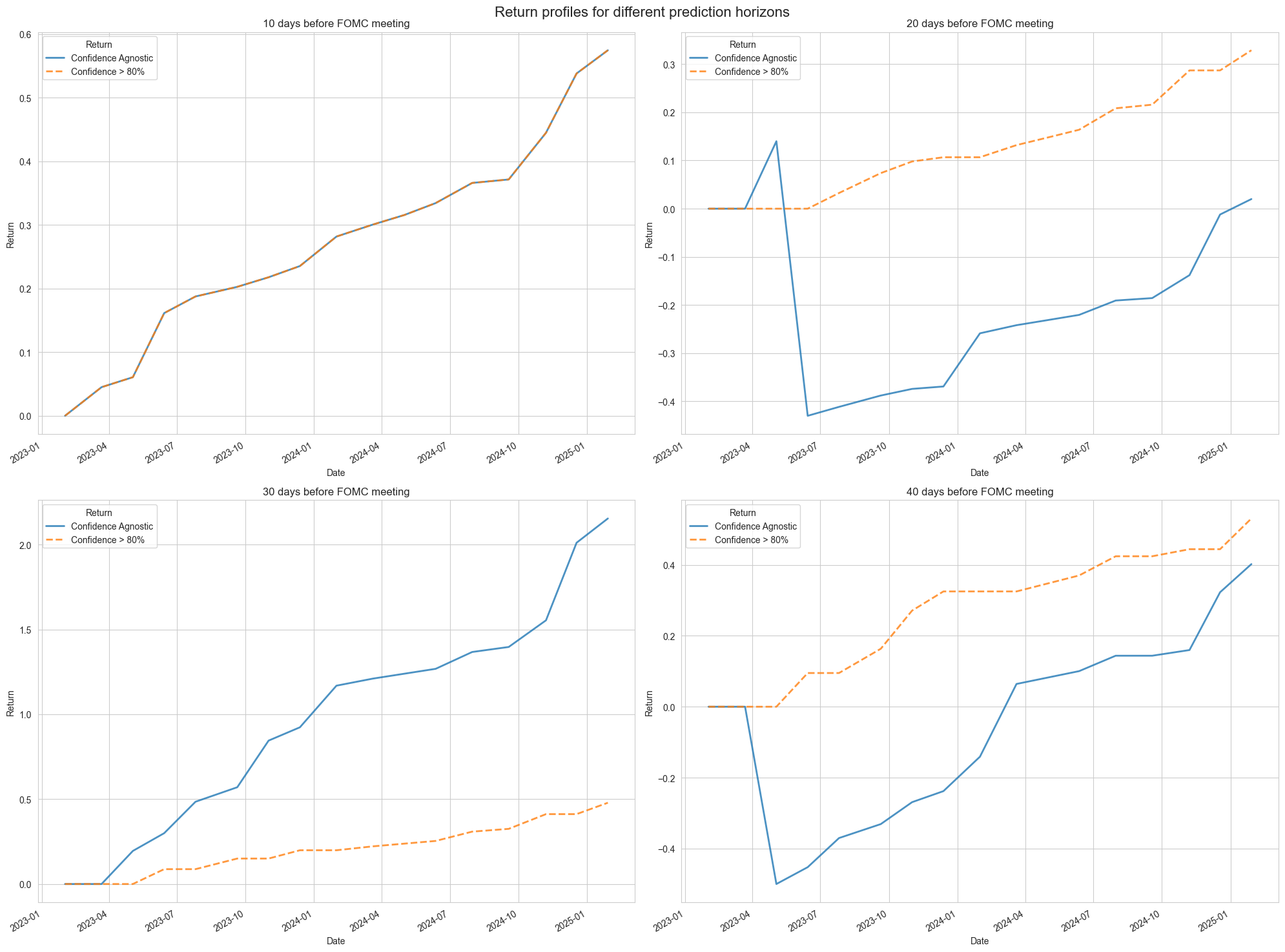

A strategy

The long view